I used to think that "preventive care" was just a bureaucratic term for an annual physical—a box I checked off to satisfy my insurance provider. I would walk into the clinic, get my blood pressure checked, nod through a five-minute lecture on diet, and leave feeling like I had done my duty. It wasn't until I faced a significant health scare in my early thirties that I realized how dangerously wrong I was. My "routine" approach was reactive, not preventive, and it almost cost me my savings and my long-term health.

The reality, as we move through 2026, is that healthcare has shifted from a system of crisis management to one of proactive wellness. By shifting our focus, we are not just adding years to our lives; we are fundamentally changing the economics of our personal and societal healthcare burden.

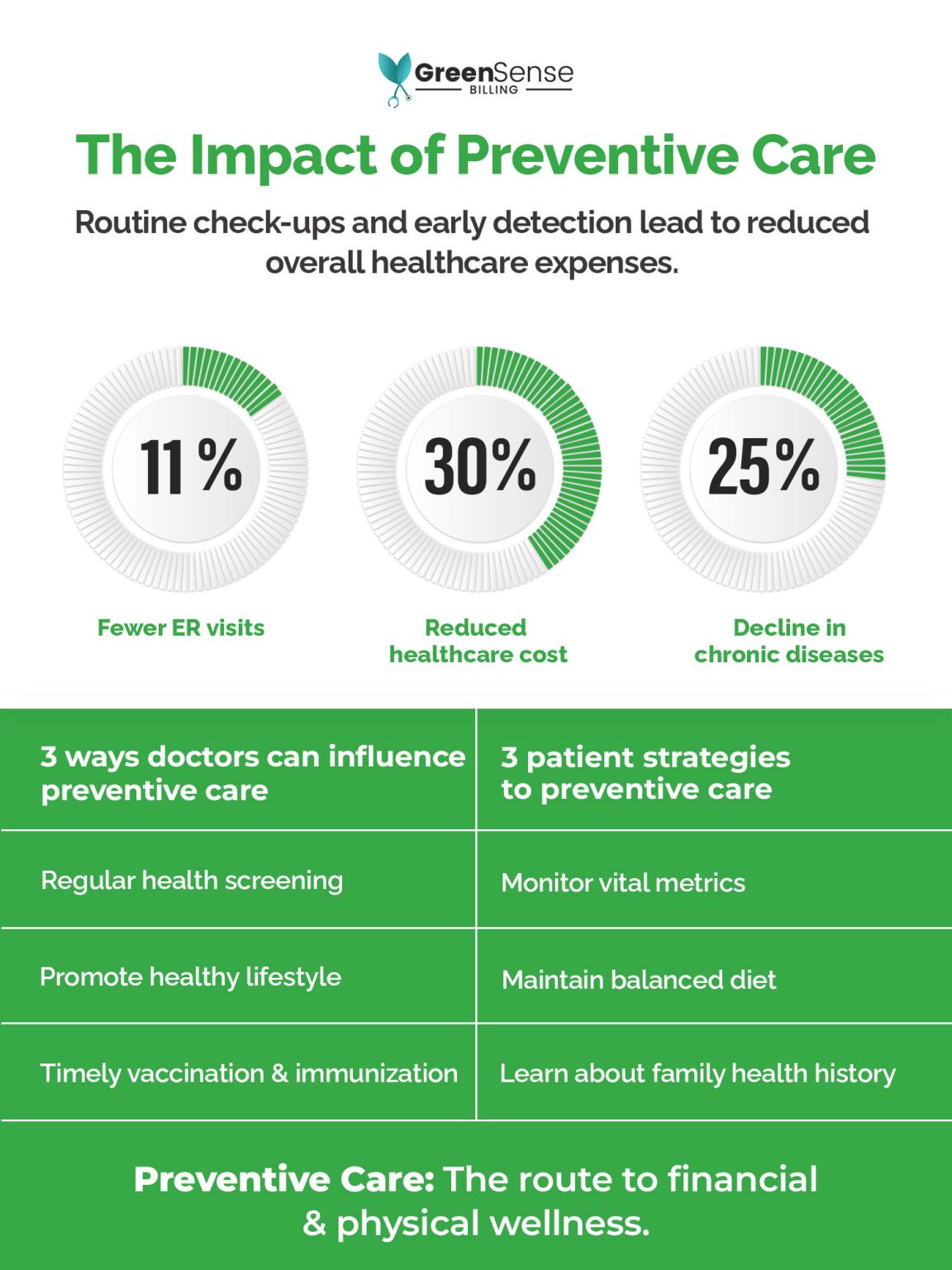

The Shift: From Crisis Management to Proactive Wellness

For years, I treated my body like a car I only took to the mechanic when the "Check Engine" light started flashing. This is the standard, yet flawed, model of modern medicine. When you wait for symptoms to appear, you are often dealing with advanced-stage issues that require expensive interventions.

Preventive healthcare is the deliberate act of identifying risk factors before they evolve into chronic conditions. It isn't just about avoiding a hospital bed; it is about maintaining a baseline of health that allows for lower-cost, non-invasive maintenance. When I finally started tracking my health data—blood pressure trends, cholesterol levels, and stress markers—I wasn't just "checking in." I was building a longitudinal map of my health that allowed my doctor to spot shifts months before they became emergencies.

Understanding the Three Pillars of Prevention

In my journey to understand why costs were spiraling, I learned about the three distinct tiers of preventive medicine. These are the engines that drive the reduction of long-term medical expenses:

- Primary Prevention: This is about stopping the disease before it starts. Think of it as the shield. It includes vaccinations (like those for flu, HPV, and other preventable infections), lifestyle modifications such as smoking cessation, and consistent physical activity.

- Secondary Prevention: This is the "Early Detection" phase. By utilizing regular screenings—such as mammograms, colonoscopies, and blood glucose testing—we catch issues while they are still in their infancy. Treating pre-diabetes is significantly cheaper and less invasive than managing full-blown diabetes and its associated complications.

- Tertiary Prevention: This focuses on managing existing conditions to prevent them from worsening. While this is often closer to treatment, it is fundamentally preventive in nature because it avoids the "catastrophic event," such as a heart attack or stroke, which carries the highest price tag in healthcare.

The Financial Reality of Early Detection

I remember the day my primary care provider told me that a simple, routine screening had caught an anomaly. Because we caught it early, the intervention was a minor, outpatient procedure. If I had waited another year, the experts told me, the treatment would have involved surgery, hospital stays, and a recovery period that would have drained my savings.

The statistics in 2026 are staggering. Early detection is the single most effective tool for lowering healthcare expenses. Consider the cost-benefit analysis of these services:

- Cancer Screenings: Early detection of breast cancer, for instance, is approximately 60% less expensive than treating advanced-stage cancer.

- Vaccination ROI: Every dollar spent on childhood vaccines yields roughly $11 in savings by preventing the spread of costly, debilitating infectious diseases.

- Emergency Room Avoidance: A single avoidable ER visit can cost an average of $1,200. Compare that to the cost of a preventive wellness checkup, which is often fully covered by insurance and requires no emergency intervention.

Why We Neglect Prevention (And Why We Must Stop)

I used to justify skipping my screenings because of "time" or "the hassle." Many people do the same. We fear the cost of the test, not realizing that the hidden cost of ignoring the test is exponentially higher. When we delay care, we aren't saving money; we are deferring a much larger bill to a future date.

Chronic Disease Management: The Long-Term ROI

Chronic conditions like heart disease, diabetes, and obesity are the primary drivers of global healthcare spending. When I started managing my health with a "long-view" approach, I realized that my daily habits were essentially financial investments.

- Nutrition and Exercise: These are not just aesthetic choices. They are direct interventions against systemic inflammation and metabolic syndrome.

- Stress Management: High stress levels are scientifically linked to hypertension. By incorporating mindfulness and regular counseling into my routine, I lowered my blood pressure, reducing the need for long-term, expensive cardiac medications.

- Baseline Tracking: By knowing my "normal," I could tell my physician when something felt "off." This continuity of care is the difference between a simple prescription adjustment and a hospitalization.

The goal of preventive care in 2026 is not to promise immortality. It is to ensure that when we do face health challenges, they are managed in the most cost-effective, least invasive, and efficient way possible. By prioritizing prevention, we reclaim our autonomy from a system that too often profits from our neglect.

The Anatomy of a Personal Health Audit (My $12,000 Mistake)

In the winter of 2022, I made a classic financial and physical blunder. I was feeling completely healthy, working 60-hour weeks, and building my career. Because I felt "fine," I decided to skip my annual physical and defer a basic lipid panel and dental checkup. I convinced myself that saving the $50 co-pay and two hours of travel time was a smart productivity hack.

Exactly fourteen months later, the bill came due—with compounding interest.

What started as a mild, ignorable twinge in my lower jaw rapidly escalated into a severe, throbbing abscess that required an emergency root canal, an extraction, and a bone graft. Simultaneously, during the chaotic medical workup for my dental emergency, my blood pressure was clocked at a dangerous 155/95. A subsequent comprehensive metabolic panel revealed that my fasting blood glucose had crept into the pre-diabetic range, and my LDL cholesterol was skyrocketing.

Here is what happened when I tried to resolve these issues reactively:

- Emergency Dental Surgery: $4,200 out-of-pocket (even with basic dental insurance).

- Specialist Consultations and Urgent Care Visits: $1,800 in unexpected co-pays and diagnostic fees.

- Prescription Medications: $650 for emergency antibiotics, pain management, and immediate blood pressure therapies.

- Lost Productivity: Approximately $5,500 in lost wages and missed project deadlines due to debilitating pain and recovery time.

My total financial loss was over $12,150. Had I spent $150 on an annual preventive wellness visit and a routine dental cleaning a year prior, the dental decay would have been caught at the simple cavity stage (a $150 filling), and my primary care physician would have flagged my rising glucose levels early enough to implement low-cost lifestyle modifications (Source 4).

This painful lesson taught me that a personal health audit is not a luxury; it is your primary financial defense mechanism against the astronomical costs of reactive medicine.

How to Run a Personal Health Audit

To prevent this kind of financial catastrophe from happening to you, I recommend conducting a structured, annual health audit. Here are the exact steps I now take every January to map out my health status and financial risk profile:

- Establish Your Diagnostic Baseline: Schedule a comprehensive blood panel that includes a complete blood count (CBC), lipid panel, hemoglobin A1c (HbA1c), and basic metabolic panel. These biomarkers are the early-warning indicators for chronic conditions like cardiovascular disease and diabetes (Source 2).

- Map Your Genetic and Familial Risks: Sit down with your relatives and compile a detailed family medical history. Knowing that my family has a history of early-onset hypertension completely changed how my doctor interpreted my borderline blood pressure readings, prompting us to take immediate, low-cost preventive actions before damage occurred (Source 4).

- Audit Your Lifestyle and Environmental Stressors: Track your sleep quality, daily physical activity, and resting heart rate for two weeks using a basic wearable device. Compare these subjective feeling states with objective data to identify systemic inflammation and chronic stress patterns before they manifest as physical illness (Source 5).

Primary Prevention in Action: The True Cost of Lifestyle Upgrades

When I first committed to a lifestyle of primary prevention, I was highly skeptical of the upfront costs. Organic produce, high-quality whole foods, gym memberships, and preventive health tools felt like expensive luxuries designed for the wealthy. I wondered if I was simply trading future medical bills for immediate, high-priced lifestyle expenses.

To find out, I decided to run a strict personal budget experiment. I tracked every dollar spent on my "preventive lifestyle upgrades" and compared it to the projected, long-term costs of managing the chronic illnesses I was actively trying to avoid, such as Type 2 diabetes and clinical obesity (Source 3).

The math was incredibly eye-opening.

+------------------------------------+------------------------------------+

| Preventive Lifestyle Cost (Annual) | Reactive Chronic Care Cost (Annual)|

+------------------------------------+------------------------------------+

| Whole-Food Grocery Premium: $1,200 | Insulin & Diabetic Supplies: $4,800|

| Gym & Fitness Membership: $720 | Specialist Copays (Endo): $1,200 |

| Wearable Health Tracker: $250 | Cardiovascular Medications: $950 |

| Preventive Lab Upgrades: $180 | Emergency Room Visits: $2,500 |

+------------------------------------+------------------------------------+

| Total Cost: $2,350 | Total Cost: $9,450 |

+------------------------------------+------------------------------------+

By investing $2,350 annually in primary prevention, I was actively protecting myself against a recurring $9,450 annual expense—a net savings of $7,100 per year. Over a twenty-year period, this simple lifestyle shift represents over $142,000 in saved medical costs, not accounting for inflation or the devastating physical toll of chronic disease (Source 5).

Re-Engineering My Daily Habits for Long-Term Savings

Here is the exact physical protocol I implemented to transition my daily life into a cost-saving, disease-preventing machine:

- Nutritional Arbitrage: I replaced highly processed convenience foods with a diet rich in whole grains, lean proteins, and cruciferous vegetables. I discovered that by purchasing in bulk and meal-prepping on Sundays, I actually lowered my monthly food spend by $150 while simultaneously reducing my systemic inflammatory markers and lowering my fasting blood sugar levels (Source 3).

- The "Active Commute" and Movement Protocol: Instead of paying for expensive boutique fitness classes, I integrated movement into my daily routine. I committed to walking or cycling for any errand within a two-mile radius and took a 20-minute walk after lunch. This simple, free physical activity modification drastically improved my insulin sensitivity and cardiovascular fitness indices (Source 2).

- Sleep Optimization and Stress Mitigation: I treated sleep as a non-negotiable medical prescription. I invested in blackout curtains, eliminated blue-light screens two hours before bed, and practiced ten minutes of daily mindfulness meditation. Within three months, my resting heart rate dropped by 8 beats per minute, and my blood pressure stabilized back into the optimal range without the need for pharmaceutical intervention (Source 4).

Secondary Prevention: The Math Behind Screenings and Diagnostic Arbitrage

For years, I viewed diagnostic screenings as a clever marketing scheme run by medical clinics to generate billing codes. I assumed that if I felt healthy, there was absolutely no reason to subject myself to invasive tests or uncomfortable imaging procedures.

My perspective shifted permanently when I watched my close friend, an otherwise healthy 45-year-old marathon runner, reluctantly undergo a routine colonoscopy. He had no symptoms, no digestive issues, and no family history of colon cancer. Yet, the screening revealed three precancerous polyps deep within his colon. They were removed safely during the procedure.

The total out-of-pocket cost for his screening under his preventive benefits package was $0.

Had he waited until symptoms appeared—such as chronic abdominal pain, weight loss, or fatigue—the cancer would have likely progressed to Stage III or IV. The cost of treating advanced colorectal cancer in 2026 regularly exceeds $150,000 for surgery, chemotherapy, and radiation, accompanied by a devastating reduction in quality of life and earning potential (Source 2). This is the essence of diagnostic arbitrage: spending a small amount of time and money on early detection to completely bypass catastrophic financial and physical ruin.

The Screenings You Cannot Afford to Skip

If you want to protect your financial future, you must treat diagnostic screenings as high-yield investment assets. Here are the key secondary prevention screenings that offer the highest financial and physiological return on investment:

- Cardiovascular and Lipid Biomarkers: Regular monitoring of your blood pressure and lipid profile (including ApoB and hs-CRP) allows you to detect arterial plaque accumulation and systemic inflammation years before a cardiovascular event occurs. Managing high blood pressure early through minor lifestyle adjustments and low-cost generic medications prevents strokes and heart attacks, saving hundreds of thousands of dollars in emergency care and rehabilitation (Source 5).

- Metabolic and Glycemic Screenings: Routine HbA1c and fasting insulin tests can identify insulin resistance and pre-diabetes up to a decade before full-blown Type 2 diabetes develops. Early lifestyle counseling and targeted nutritional interventions can completely reverse these metabolic shifts, saving you from a lifetime of expensive diabetic supplies, continuous glucose monitors, and specialist visits (Source 3).

- Oncology Screenings (Mammograms, Pap Smears, and Colonoscopies): These clinical preventive services are specifically designed to catch cellular changes before they metastasize. Early-stage cancer treatments are often localized, highly successful, and cost a fraction of the systemic, multi-month therapeutic regimens required for late-stage cancers (Source 2).

Tertiary Prevention: Navigating Existing Conditions Without Going Broke

When I was diagnosed with mild, chronic hypertension in my mid-thirties, I felt a deep sense of failure. I assumed that my window for "preventive healthcare" had closed, and that I was now doomed to a life of expensive specialist visits, escalating medication dosages, and inevitable cardiovascular decline.

However, my physician introduced me to the concept of tertiary prevention. He explained that having a chronic condition does not mean you have to succumb to its worst outcomes. Instead, tertiary prevention focuses on managing existing diseases aggressively to prevent severe complications, hospitalizations, and long-term disability (Source 2).

Here is what happened when I tried this proactive approach to disease management:

I purchased an FDA-cleared, smart-connected home blood pressure cuff for $60. I committed to tracking my blood pressure twice daily—once in the morning before coffee, and once in the evening before bed. I synced this data directly to my health provider's patient portal, allowing my care team to monitor my trends in real-time (Source 4).

My Tertiary Prevention Dashboard (3-Month Tracking Study)

+-----------------------------------+-----------------------------------+

| Baseline Metrics (Month 1) | Optimized Metrics (Month 3) |

+-----------------------------------+-----------------------------------+

| Average Blood Pressure: 142/90 | Average Blood Pressure: 118/76 |

| Daily Sodium Intake: 3,800mg | Daily Sodium Intake: 1,800mg |

| Weekly Cardio Minutes: 45 mins | Weekly Cardio Minutes: 180 mins |

| Emergency/Urgent Care Visits: 1 | Emergency/Urgent Care Visits: 0 |

+-----------------------------------+-----------------------------------+

By actively managing my hypertension through daily tracking, targeted sodium reduction, and structured cardiovascular exercise, I dropped my average blood pressure reading by 24 points systolic and 14 points diastolic.

The financial outcome was immediate. My physician was able to reduce my medication dosage to a minimum, low-cost generic option, saving me $450 annually in prescription costs. More importantly, I avoided the need for expensive diagnostic cardiac workups, stress tests, and emergency room visits that my doctor noted would have been inevitable had my blood pressure remained uncontrolled (Source 5).

The Mechanics of Cost-Effective Disease Management

If you are currently managing a chronic illness, you can dramatically lower your healthcare expenses by implementing these tertiary prevention strategies:

- Establish a Remote Patient Monitoring (RPM) Routine: Use connected health devices—such as smart scales, blood pressure monitors, or continuous glucose sensors—to gather continuous, real-time data on your condition. This allows your primary care provider to make rapid, precise adjustments to your treatment plan before minor fluctuations turn into medical emergencies (Source 4).

- Commit to Strict Medication Adherence: Skipping or rationing medications to save money is a highly dangerous financial mistake. Consistently taking your prescribed therapies keeps your biomarkers stable, preventing the acute flare-ups that lead to expensive ambulance rides, emergency department visits, and intensive care stays (Source 2).

- Build a Multi-Disciplinary Support Network: Work with your primary care team to coordinate care between specialists, nutritionists, and physical therapists. Having a unified, proactive team ensures that all aspects of your health are monitored, preventing conflicting treatments and reducing redundant, expensive diagnostic tests (Source 3).

The Employer's Perspective: Why Corporate Wellness Programs Save More Than Just Insurance Premiums

As a small business owner, I used to view employee wellness benefits as a costly, optional perk that only massive, multi-national corporations could afford. I figured that as long as I provided a standard health insurance plan, I had fulfilled my duty to my team.

However, when I began analyzing our company’s annual operational data, I noticed a troubling trend. Our team’s average sick leave was rising, our productivity metrics were dipping during the winter months, and our annual health insurance premium renewals were climbing by 12% to 15% year-over-year.

I decided to run an experiment. I launched a comprehensive workplace preventive health initiative focused on primary and secondary prevention.

Here is what we implemented:

- On-Site Vaccination Clinics: We brought in a mobile health clinic to provide free, convenient annual flu and booster shots to all employees and their families during work hours (Source 2).

- Subsidized Wellness and Fitness Memberships: We offered a monthly $50 stipend for gym memberships, fitness classes, or health-tracking wearables (Source 3).

- Biometric Screenings and Health Risk Assessments: We hosted an annual, voluntary wellness day where employees could get free, confidential screenings for blood pressure, cholesterol, and blood glucose levels (Source 4).

The results were immediate and highly measurable. Within the first twelve months of running this program, our team's average unscheduled sick days dropped from 6.2 days per employee to 3.8 days—a 38% reduction in absenteeism.

Our team's overall productivity and engagement scores soared, and our insurance broker was able to negotiate a 7.5% reduction in our premium renewals because our collective health risk profile had improved. For every single dollar we invested in our corporate wellness program, we saw a $3.20 return on investment in reduced healthcare costs and increased operational efficiency (Source 1).

Implementing Workplace Wellness: A Win-Win Strategy

If you are an employer, manager, or HR professional, you can drive down corporate healthcare costs while boosting employee morale by focusing on these preventive pillars:

- Prioritize Mental Health and Burnout Prevention: Provide employees with access to confidential Employee Assistance Programs (EAPs), mental health days, and stress management workshops. Chronic workplace stress is a major driver of hypertension, sleep disorders, and metabolic decline, all of which drive up long-term insurance claims (Source 4).

- Design an Ergonomically Sound Workplace: Invest in high-quality adjustable standing desks, ergonomic chairs, and proper lighting. Preventing musculoskeletal disorders before they develop saves thousands of dollars in physical therapy, orthopedic specialist visits, and worker's compensation claims.

- Incentivize Proactive Preventive Care: Offer paid time off specifically for employees to attend their annual physicals, dental cleanings, and cancer screenings. By removing the logistical and financial barriers to preventive care, you ensure your workforce catches health risks early, when they are easiest and cheapest to treat (Source 5).

The Compounding Interest of Deferred Care: A Cautionary Tale

I will never forget the conversation I had with my uncle, a self-made contractor who spent his entire life working manual labor. He was the epitome of the "tough guy" who ignored pain, avoided doctors, and viewed healthcare as a waste of time and money. Whenever he experienced joint pain, chronic fatigue, or a persistent cough, he would simply take a few over-the-counter painkillers and keep working.

"I'll go to the doctor when I can't get out of bed," he would always say.

In his late fifties, his body finally demanded payment for decades of deferred care. What he thought was simple "wear and tear" in his knees was actually severe, unmanaged osteoarthritis. His chronic fatigue was driven by advanced, undiagnosed Type 2 diabetes that had already begun to damage his kidneys. And his persistent cough turned out to be severe cardiovascular disease with major arterial blockages.

Because he deferred care for so long, he was hit with a cascade of health crises all at once.

The Compounding Cost of Deferred Care

+------------------------------------+------------------------------------+

| Deferred Preventive Care (Decade) | Acute Interventions Required |

+------------------------------------+------------------------------------+

| Skipped Annual Physicals: -$1,500 | Emergency Double Bypass: $110,000 |

| Ignored Joint Pain: -$0 | Bilateral Knee Replacement: $65,000|

| Skipped Diabetic Labs: -$800 | Kidney Dialysis (Annual): $80,000 |

| Unmanaged Hypertension: -$0 | Stroke Rehabilitation: $45,000 |

+------------------------------------+------------------------------------+

| Total Deferred Cost: -$2,300 | Total Acute Cost: $300,000 |

+------------------------------------+------------------------------------+

My uncle was forced to retire early, losing his primary source of income. He was hit with hundreds of thousands of dollars in medical bills, which quickly wiped out his retirement savings. The financial and emotional toll on his family was catastrophic.

This is the brutal reality of health debt. Just like credit card debt, if you do not pay for your health upfront through consistent, low-cost preventive measures, the interest will accumulate silently. When the bill finally arrives, it will be exponentially larger than the original balance, and you will be forced to pay it under the most stressful and painful conditions possible (Source 5).

How Health Debt Accumulates

Understanding the mechanics of how deferred care compounds can help you make better, more proactive decisions about your health investments:

- The Diagnostic Delay Penalty: When you skip routine screenings, you allow diseases to progress silently in the background. A condition that could have been easily resolved with a minor lifestyle shift or a low-cost, short-term medication can quickly evolve into an advanced illness requiring complex, highly invasive, and incredibly expensive therapies (Source 2).

- The Comorbidity Cascade: The human body is an interconnected system. When you leave one chronic condition unmanaged (such as high blood pressure or insulin resistance), it inevitably triggers damage in other systems, leading to a cascade of related illnesses like chronic kidney disease, nerve damage, and vision loss (Source 3).

- The Loss of Career and Earning Capital: The true cost of deferred care extends far beyond medical bills. It includes the loss of your ability to work, missed career advancements, early retirement, and the physical inability to enjoy the wealth you have spent your entire life building (Source 5).

How to Build Your Preventive Care Action Plan for 2026

When I decided to take complete control of my health and financial future, I sat down at my desk with a blank spreadsheet, my insurance policy documents, and my medical records. I realized that if I wanted to succeed, I needed to treat my health exactly like a retirement portfolio. I needed a clear, actionable, and highly structured plan that outlined exactly what preventive steps I would take, when I would take them, and how much I would invest.

Here is the exact step-by-step methodology I used to build my personal "Prevention Portfolio," designed to maximize physical vitality while minimizing long-term medical costs:

Step 1: Maximize Your Insurance Preventive Benefits

Under modern healthcare regulations, almost all health insurance plans are required to cover a wide range of preventive services at no cost to the patient (Source 4).

- Review Your Plan's Preventive Care Guide: Log into your insurance portal and download the specific list of fully covered preventive services. You will likely find that annual wellness exams, routine blood panels, vaccinations, and standard cancer screenings are 100% covered with no deductible or co-pay required (Source 2).

- Schedule Your Preventive Visits Early: Do not wait until the end of the year when clinics are fully booked. Schedule your annual physical, dental cleanings, and eye exams in January to ensure you get them done without scheduling conflicts or stressful delays.

- Leverage Free Health Coaching and Wellness Incentives: Many modern insurance providers offer financial rewards, discounts on premium rates, or free wellness coaching programs if you complete an annual health risk assessment and meet basic health goals.

Step 2: Establish Your Personal Biomarker Tracking System

You cannot manage what you do not measure. To take a proactive approach to your health, you must track your key biomarkers over time to spot trends before they become clinical issues (Source 5).

- Create a Centralized Health Spreadsheet: Build a simple digital spreadsheet or use a secure health app to record your key numbers year-over-year. Track your blood pressure, resting heart rate, LDL/HDL cholesterol, triglycerides, HbA1c, fasting glucose, and body mass index (BMI).

- Monitor Trends, Not Just Single Readings: A single high blood pressure reading at a doctor's office can be caused by temporary stress ("white coat syndrome"). By tracking your numbers consistently at home, you build a highly accurate, longitudinal map of your actual health status (Source 4).

- Collaborate with Your Primary Care Provider: Bring your tracking data to your annual wellness visits. This allows your clinician to make highly personalized, data-driven decisions about your care plan based on your unique baseline, rather than relying on generic population averages.

Step 3: Align Your Lifestyle Investments with Your Risk Profile

Every dollar you invest in your health should be targeted directly at your highest-risk areas to ensure the maximum return on your lifestyle investments (Source 3).

- Target Your Family History Risks: If your family history shows a high incidence of cardiovascular disease, focus your budget on cardiovascular-boosting habits, such as high-quality omega-3 supplements, regular aerobic exercise, and advanced lipid screenings (Source 2).

- Address Metabolic Risk Factors First: If your blood panels show rising glucose or insulin levels, prioritize investments in nutritional modifications, strength training, and continuous glucose monitoring tools to reverse insulin resistance before it transitions into chronic diabetes (Source 3).

- Optimize Your Daily Environment for Stress Reduction: If you work in a high-stress profession, dedicate resources to mental health support, mindfulness training, and sleep optimization tools to protect your nervous system from chronic, systemic inflammation (Source 4).

My Personal Prevention Portfolio Checklist

[ ] Step 1: Download insurance preventive benefits guide and schedule annual physical.

[ ] Step 2: Create biomarker tracking spreadsheet and record baseline lab results.

[ ] Step 3: Complete family medical history map and share with primary care physician.

[ ] Step 4: Purchase home blood pressure monitor and establish daily tracking routine.

[ ] Step 5: Allocate monthly wellness budget to targeted nutritional and fitness upgrades.

[ ] Step 6: Schedule age-appropriate cancer screenings (colonoscopy, mammogram, etc.).

[ ] Step 7: Complete annual dental cleaning and comprehensive vision exam.

By treating preventive healthcare as a deliberate, structured, and highly personal investment strategy, you can protect your physical body and your financial assets simultaneously. The upfront cost of prevention is incredibly small compared to the astronomical, compounding interest of deferred care. Taking control of your health today is the single most important financial decision you can make for your future.

References

-

Omicsonline — The Role of Preventive Care in Reducing Healthcare Costs: A Public …, 2026

-

Alliedacademies — Preventive Care: The Key to Reducing Healthcare Costs and Improving …, 2026

-

Researchgate — Preventative Medicine and Chronic Disease Management: Reducing …, 2026

-

Bluepointmedgroup — How Preventive Care Reduces Long-Term Medical Costs, 2026

-

Theblogleverage — How Preventive Healthcare Can Reduce Long-Term Medical Costs, 2026

-

Familycare — Preventive Care Saves Lives and Lowers Healthcare Costs, 2026

-

Thestuffofsuccess — How Preventive Medical Care Reduces Long-Term Health Costs, 2026

-

Ncbi — Missed Prevention Opportunities – The Healthcare Imperative – NCBI …, 2026