It was 3:00 AM on a rainy Tuesday in January 2026 when my phone rang—the call every adult child dreads. My 68-year-old father had been rushed to the emergency room with severe chest pains. As I sat in the sterile hospital waiting room, clutching a plastic cup of lukewarm coffee, a administrative coordinator handed me a clipboard stacked with insurance verification forms.

That was the exact moment I realized how dangerously unprepared we were. I thought we had a great plan in place, but I quickly discovered that our understanding of comprehensive healthcare plans for senior citizens was filled with massive, expensive blind spots.

Over the next six months, I went on an obsessive quest to master the senior healthcare landscape. I read hundreds of pages of policy fine print, interviewed certified insurance experts, and built complex spreadsheets comparing premiums, co-pays, and network restrictions.

Here is the exact blueprint of what I discovered, the costly mistakes I made along the way, and how you can secure the absolute best medical coverage for yourself or your aging parents in 2026. This includes understanding the critical role of preventive care services in maintaining long-term health.

The Costly Mistakes I Made in the Beginning

When I first took over my parents' healthcare planning, I fell into several common traps. I want to share these openly so you do not have to pay the same financial and emotional price that I did.

Mistake 1: Falling for the "Senior-Specific Plan" Marketing Trap

I initially assumed that any plan labeled "Senior Citizen Special" was automatically the best choice. This is a massive misconception.

When I looked closely at senior-specific policies, I found they often came loaded with built-in limits like co-pays, room rent caps, and strict sub-limits. These clauses drastically reduce how much the insurer pays, leaving you to cover the rest out of pocket.

I learned that if a senior can medically qualify, a comprehensive health insurance plan is almost always the superior starting point. Comprehensive plans offer stronger coverage growth features like restoration benefits and cumulative bonuses, which are vital as medical costs continue to rise.

Mistake 2: Ignoring the "Waiting Period" Fine Print

My father has managed type-2 diabetes for over a decade. I foolishly believed that buying a premium policy meant his treatments would be covered immediately.

I was wrong. Many policies impose a waiting period of 2 to 4 years for pre-existing conditions before they pay a single dime for related treatments. In 2026, finding plans with shorter waiting periods—or paying a slightly higher premium to waive them entirely—became my top priority.

Mistake 3: Treating All Deductibles and Co-pays Equally

I initially chose a plan with a lower monthly premium because it had a "modest" 20% co-pay. I did not do the math on the total cost-sharing.

A 20% co-pay on a minor outpatient visit is manageable. But when my father required a major joint replacement surgery costing thousands of dollars, that 20% co-pay translated into a massive, unexpected bill.

I learned to prioritize plans with zero co-pay options, even if the monthly premiums were higher, and always checked for a reasonable out-of-pocket maximum to cap my financial risk.

My Physical Steps to Auditing Our Healthcare Needs

Before you spend a single dollar on a premium, you must conduct a thorough audit. Here is the exact, step-by-step physical process I used to evaluate my family's medical requirements.

Step 1: Create a Comprehensive Medical Diary

I sat down with my parents and listed every single medical touchpoint they experienced over the previous 24 months. I documented:

- Every prescription medication, including exact dosages and monthly costs, and strategies for ensuring medication adherence.

- All recurring specialist visits (cardiologists, endocrinologists, physical therapists), noting any specific chronic disease management programs or therapies.

- The frequency of diagnostic tests like blood work, MRIs, and X-rays.

- Any planned or highly probable surgeries (such as cataract removal or joint replacements).

Step 2: Build a Provider and Hospital Network Map

I made a list of every doctor, hospital, and clinic my parents trusted. I then cross-referenced this list with the provider directories of major insurance carriers.

Keeping your trusted doctors is crucial for continuity of care. I quickly eliminated any plan that would force my parents to change their primary care physician or cardiologist.

Step 3: Calculate the Total Cost of Ownership (TCO)

Do not just look at the monthly premium. I built a spreadsheet to calculate the Total Cost of Ownership for each plan using this formula:

$$text{TCO} = (text{Monthly Premium} times 12) + text{Annual Deductible} + text{Estimated Out-of-Pocket Co-pays for Prescriptions and Visits}$$

This simple math revealed that some "expensive" plans with high premiums were actually much cheaper over a full year because they featured low deductibles and comprehensive drug coverage.

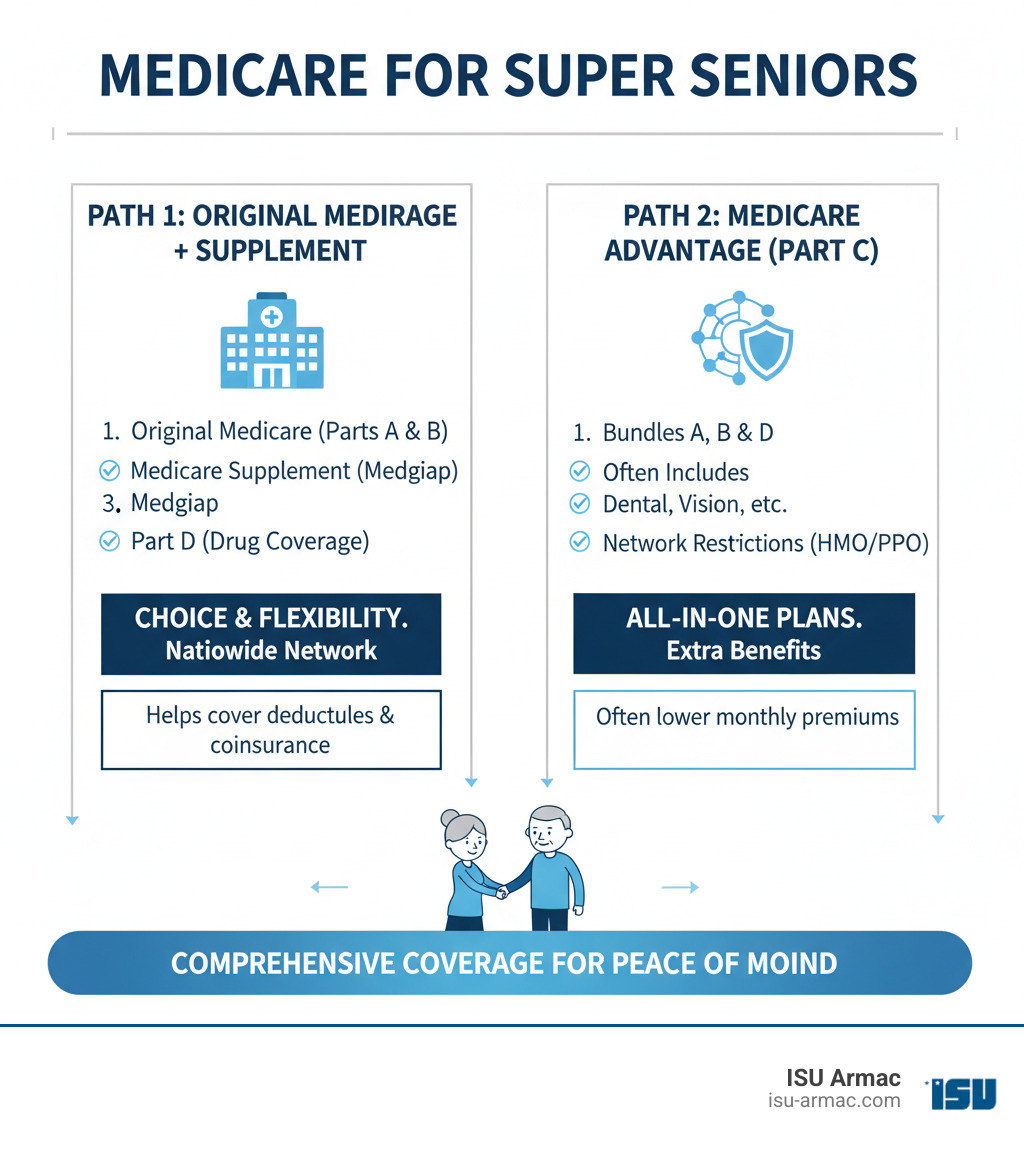

Deciphering the United States Senior Healthcare Maze in 2026

If you are navigating the system in the United States, you are primarily dealing with Medicare, its various parts, and supplemental private options. Understanding the Annual Enrollment Period (AEP), typically from October 15 to December 7 each year, is crucial for making informed choices or changes to your Medicare coverage. Here is what I discovered when setting up my mother's coverage.

Medicare Parts A and B: The Foundation (Original Medicare)

Original Medicare is a federal health insurance program for individuals aged 65 and older. It is divided into two main parts:

- Medicare Part A (Hospital Insurance): This covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care. For most seniors who paid Medicare taxes while working, Part A has no monthly premium.

- Medicare Part B (Medical Insurance): This covers outpatient services, doctor visits, preventive services, and medical supplies. Part B requires a monthly premium, which is adjusted annually based on income.

While Original Medicare is a fantastic foundation, I quickly realized it has a massive vulnerability: it has no out-of-pocket maximum. If you experience a catastrophic health event, your 20% co-insurance responsibility under Part B could financially ruin you.

Medicare Part C: The Medicare Advantage Alternative

To avoid the gaps in Original Medicare, we looked closely at Medicare Part C (Medicare Advantage). These plans are offered by private, Medicare-approved companies.

┌─────────────────────────────────────────┐

│ Original Medicare │

│ (Part A + Part B) │

└────────────────────┬────────────────────┘

│

Is there a gap in coverage? Yes.

│

┌─────────────────────────┴─────────────────────────┐

▼ ▼

┌───────────────────────────┐ ┌───────────────────────────┐

│ Medicare Part C │ │ Medigap Plan │

│ (Medicare Advantage) │ │ (Supplemental Policy) │

├───────────────────────────┤ ├───────────────────────────┤

│ • Private network (HMO/PPO)│ │ • Works with Part A & B │

│ • Often includes Part D │ │ • Covers deductibles/copay│

│ • May have copays/limits │ │ • Freedom of doctor choice│

└───────────────────────────┘ └───────────────────────────┘

Medicare Advantage plans bundle Part A, Part B, and usually Part D (prescription drugs) into a single plan. Many also offer extra perks like dental, vision, and wellness programs.

However, I discovered a major catch: network restrictions. Under Medicare Advantage, you are generally limited to a specific network of doctors (HMO or PPO). If you go out of network, you may pay the full cost yourself. For my parents, who love to travel, this restriction was a dealbreaker.

Medicare Part D: Prescription Drug Coverage

If you stick with Original Medicare, you must purchase a standalone Medicare Part D plan to cover your prescription medications.

I learned that every Part D plan has a formulary—a specific list of covered drugs organized into tiers. I spent hours typing my father’s medications into the Medicare plan finder tool to ensure we chose a plan that placed his expensive cardiac medications in a lower, highly subsidized tier.

Medigap (Medicare Supplement Insurance)

This was my favorite discovery. Medigap policies are private insurance plans designed to fill the "gaps" in Original Medicare. They pay for deductibles, co-pays, and co-insurance.

If you have Original Medicare and a Medigap plan, your out-of-pocket medical costs can drop to near zero. The downside? The monthly premiums are higher, and you must purchase a separate Part D plan for your prescriptions. But for peace of mind, Medigap is incredibly hard to beat.

Evaluating Top Private Carriers in the US

During my research, I thoroughly analyzed the offerings of the leading private health insurance companies in 2026. Here is my subjective take on each:

Kaiser Permanente: The Integrated Care Champion

If you live in a region served by Kaiser Permanente, their integrated care model is highly impressive.

- The Experience: Everything is under one roof. Your doctors, specialists, labs, and pharmacy operate within the same system and share a single electronic medical record.

- The Verdict: This model makes healthcare navigation and care coordination incredibly smooth for seniors. However, you must use Kaiser's facilities and doctors, typical of an HMO model. If you have a highly specialized external doctor you refuse to leave, this will not work for you.

Blue Cross Blue Shield (BCBS): The Network Giant

BCBS is legendary for its massive, nationwide provider network.

- The Experience: Almost every doctor and hospital in the United States accepts Blue Cross Blue Shield.

- The Verdict: If your senior travels frequently or splits their time between different states, a BCBS plan (especially a Medigap plan) offers unparalleled freedom and peace of mind, often resembling a PPO structure.

UnitedHealthcare: The Industry Leader

UnitedHealthcare is the largest health insurer in the US and partners directly with AARP for Medicare plans.

- The Experience: They offer an extensive array of Medicare Advantage, Medigap, and Part D plans. They also provide short-term and TriTerm medical plans for those transitioning into retirement before age 65.

- The Verdict: Their customer service portal is highly advanced, and their wellness perks are excellent. They are a highly reliable, stable option for senior coverage.

Oscar Health & Ambetter: The Tech-Forward, Budget-Friendly Disrupters

If you are looking for affordable premiums and modern digital tools, these carriers are worth a look.

- The Experience: Both Oscar and Ambetter focus heavily on telehealth services, user-friendly mobile apps, and direct cash rewards for completing wellness programs.

- The Verdict: These plans are excellent for relatively healthy seniors who are comfortable using smartphones and want to keep their monthly premiums as low as possible.

State-Level Support: Medicaid and Texas Programs

During my research journey, I also had to help a low-income relative locate healthcare assistance. This led me to explore state-sponsored programs.

In Texas, the Texas Health and Human Services (HHS) department administers programs specifically designed for low-income seniors.

- Medicaid for Seniors: This program provides essential health coverage and can help pay for Medicare premiums, deductibles, and co-payments through federal Medicare Savings Programs (MSPs).

- Long-Term Care Services: Texas HHS offers programs that assist with nursing home care, assisted living, and home-based personal care services.

If your household income is limited, I highly recommend contacting your state's health and human services department. The application process can be tedious, but the financial relief is life-changing.

Going Global: Navigating Senior Health Insurance in India

My family's healthcare journey is not limited to the United States. I also manage the healthcare plans for my aging uncle who resides in Delhi, India.

Navigating the Indian private health insurance market in 2026 was an entirely different beast. I quickly discovered that nearly one in three hospitalizations in India involves someone aged 60 or older, according to Household Health data collected by the Ministry of Statistics. This makes securing comprehensive coverage early absolutely critical.

The Battle: Comprehensive Plans vs. Senior-Specific Plans

In India, the temptation to buy a "Senior Citizen" branded plan is incredibly high because they are heavily marketed. However, my research showed that these plans are often packed with restrictive clauses.

Instead, I looked for comprehensive health plans that allowed entry at older ages. These plans have fewer built-in restrictions, meaning your out-of-pocket expenses during a medical emergency are significantly lower.

My Deep Dive into HDFC ERGO's Optima Secure

After analyzing dozens of Indian health insurance policies, we shortlisted and ultimately purchased the Optima Secure plan by HDFC ERGO. Here is the exact math and reasoning behind my decision:

- The Cost: For my 65-year-old uncle living in Delhi, we pay ₹69,433 per year for a ₹15 lakh cover.

- The Claim Settlement Ratio: HDFC ERGO backed this policy with an impressive 96.71% average claim settlement ratio for FY 2022-25. This metric gave me immense confidence that they would actually pay out when we filed a claim.

- Tax Benefits: Under Section 80D of the Income Tax Act, the premiums we pay for his health insurance provide valuable tax deductions, which helps offset the high annual cost.

- The ₹27/Day Plan Myth: You will often see advertisements for senior plans starting at "just ₹27/day." While these entry-level plans are great for basic, budget-conscious coverage, I found they often lack the robust restoration benefits and comprehensive pre-existing condition coverage that a senior truly needs.

International Senior Health Insurance: The Expat Perspective

If you are a senior who plans to retire abroad, or if you travel internationally for months at a time, standard domestic health insurance will not cover you.

I spent several weeks researching international options for my aunt, who split her retirement between Spain and the US. This led me to Cigna Healthcare's International Health Insurance for Seniors.

Why International Plans are Different

Standard travel insurance only covers unexpected emergencies. It will not cover routine checkups, ongoing cancer treatments, or chronic disease management while you are abroad.

Cigna's international plans are specifically tailored for seniors over 60, 70, or even 80. They offer:

- Core Comprehensive Cover: Essential inpatient hospital stays, emergency treatment, and cancer care.

- Optional Modules: You can customize your plan by adding modules for outpatient care, vision and dental, and international medical evacuation.

- Global Portability: The peace of mind that you can receive top-tier medical care in almost any hospital worldwide without worrying about out-of-network penalties.

The Ultimate 2026 Senior Health Insurance Checklist

To save you from the hours of frustration I experienced, I compiled this definitive comparison checklist. Before you sign any senior healthcare contract in 2026, make sure you have clear, written answers to these seven critical questions:

1. What is the Co-payment Clause?

Is there a mandatory percentage of the hospital bill you must pay? Look for plans with 0% co-pay, or understand exactly how much you will owe on a major bill, and what your annual out-of-pocket maximum will be.

2. Are there Room Rent Limits?

Many plans cap the daily room rent at 1% of the total sum insured. If you stay in a private room that exceeds this cap, the insurer will proportionately reduce their payout for your entire hospital bill. Look for plans with no room rent caps.

3. What is the Waiting Period for Pre-Existing Diseases (PED)?

How many months or years must pass before chronic conditions (like hypertension, heart disease, or diabetes) are covered? Aim for a waiting period of 24 months or less.

4. Does the Plan Have a Restoration Benefit?

If a major illness exhausts your entire sum insured in the middle of the year, will the policy automatically restore your coverage limit for the next illness? This feature is a lifesaver for older adults.

5. What are the Sub-Limits on Common Procedures?

Does the policy limit the payout for specific surgeries like cataracts, joint replacements, or kidney stone removals? Ensure these sub-limits are high enough to cover modern private hospital costs.

6. Is Daycare Treatment Covered?

Many medical procedures no longer require an overnight hospital stay. Ensure your policy covers daycare procedures like chemotherapy, dialysis, and cataract surgeries.

7. What is the Insurer's Claim Settlement Ratio (CSR)?

Never buy from a company with a CSR below 90%. You want a carrier with a proven track record of paying claims quickly and without unnecessary bureaucratic hurdles.

Navigating the Pre-65 Gap: The Early Retirement Trap

When my brother-in-law decided to retire early at the age of 61, we popped champagne and celebrated his freedom. What we did not celebrate, however, was the terrifying realization that he was still four years away from qualifying for Medicare.

He assumed he could easily find a cheap, comprehensive plan on the open market. He was wrong. This is what I call the early retirement coverage gap, and navigating it taught me some of the most expensive lessons of my life.

The Mistake: Assuming "Short-Term" Means "Comprehensive"

In his panic over high COBRA premiums, my brother-in-law almost signed up for a highly advertised online plan that promised "affordable monthly rates." When I reviewed the fine print, I realized it was a basic short-term policy that excluded his pre-existing high blood pressure and asthma. Had he faced a medical emergency, he would have been entirely on his hook for the bills.

The Discovery: TriTerm and ACA Marketplace Options

Here is what happened when I stepped in to help him navigate this transition:

- The ACA Marketplace Route: We first looked at the Affordable Care Act (ACA) exchange. Because marketplace plans cannot deny coverage or charge more for pre-existing conditions, this was the safest option. However, without a government subsidy, the monthly premiums for a 61-year-old were shockingly high.

- The TriTerm Medical Alternative: During my research, I discovered that UnitedHealthcare offers TriTerm Medical plans in select states (Source 4). These plans are designed to provide coverage for nearly three years, making them a viable bridge for early retirees transitioning toward Medicare eligibility (Source 4).

- The Short-Term Compromise: We also looked at short-term limited duration insurance plans, which provide fast, flexible coverage if you temporarily lack benefits (Source 4).

My Step-by-Step Strategy for Early Retirees

If you are planning to retire before age 65, do not leave your health coverage to chance. Here is the exact checklist we used to secure his transition:

- Calculate the COBRA Runway: Determine if you can stay on your employer’s group health plan for up to 18 months. It will be expensive because you pay the full premium, but the coverage remains identical to what you had.

- Map Out the ACA Enrollment Windows: If you lose your job-based coverage, you qualify for a Special Enrollment Period (SEP) on the healthcare.gov marketplace. You must apply within 60 days of losing your coverage.

- Evaluate TriTerm Options: If you are relatively healthy and live in a state that allows them, check if a TriTerm Medical plan fits your budget as a bridge to age 65 (Source 4).

- Confirm Pre-Existing Condition Coverage: Never cancel an existing policy until you have written confirmation that your new plan covers your current medications and chronic conditions.

The Dental, Vision, and Hearing Blindspot

One of the most shocking discoveries I made during my father's transition to Medicare was the ancillary benefit blindspot.

My father had a severe toothache and needed a root canal, followed by a crown. A few weeks later, his audiologist confirmed he needed a new pair of hearing aids. I confidently walked into the clinic, handed them his Original Medicare card, and was met with polite headshakes.

Original Medicare (Parts A and B) does not cover routine dental care, cleanings, fillings, dentures, routine eye exams, eyeglasses, or hearing aids (Source 1).

The Costly Reality of Out-of-Pocket Care

Without coverage, we were staring down a massive bill:

- Root Canal and Crown: $1,800

- Premium Hearing Aids: $4,500

- Routine Eye Exam and Bifocals: $450

I realized we had to find a systematic way to cover these essential services without draining his retirement savings.

How We Solved the Blindspot

I spent three days comparing solutions, and here is how we structured his ancillary coverage:

- Standalone Dental and Vision Plans: We researched dedicated dental plans designed specifically for seniors (Source 1, Source 5). These plans require a separate monthly premium but offer structured copays and network discounts for major procedures.

- The Medicare Advantage (Part C) Pivot: We discovered that many private Medicare Advantage plans from carriers like UnitedHealthcare and Kaiser Permanente bundle dental, vision, and hearing benefits directly into their plans (Source 1).

- Discount Programs and Community Clinics: For his hearing aids, we bypassed traditional retail clinics and utilized a specialized hearing aid discount program affiliated with his senior advocacy group, saving him over $2,000 on the devices.

What to Look For in a Senior Dental Plan

If you are shopping for standalone dental plans for a senior citizen, look for these specific features (Source 5):

- No Waiting Periods for Major Services: Many cheap plans make you wait 12 to 18 months before they will pay for a crown, bridge, or root canal. Avoid these if you need immediate work.

- High Annual Maximums: Most dental plans cap their annual payout at $1,000 or $1,500. For seniors, look for premium plans that offer a $3,000 to $5,000 annual maximum.

- Implants and Dentures Coverage: Ensure that major restorative work, including prosthodontics, is explicitly covered in the policy details.

Demystifying the Underwriting Process: How I Got My 72-Year-Old Aunt Approved

When my aunt decided to switch from a Medicare Advantage plan back to Original Medicare with a Medigap supplement at age 72, we ran straight into a brick wall: medical underwriting.

Many seniors do not realize that you only have a guaranteed right to buy a Medigap policy during your initial six-month Medicare Open Enrollment Period (which starts the month you turn 65 and enroll in Part B). If you try to buy or switch plans later, private insurance companies can look at your medical history, charge you higher premiums, or deny you coverage altogether (Source 2).

The Physical Steps of the Underwriting Process

Watching my aunt go through this process was eye-opening. Here is exactly what the insurance company did to evaluate her risk:

- The Extensive Health Questionnaire: We had to fill out a 15-page application detailing every medical diagnosis, surgery, hospital stay, and prescription drug she had taken over the past ten years.

- The Prescription Database Check: The underwriters ran her Social Security number through a national prescription database to verify if she was taking medications for undisclosed conditions like heart disease or diabetes.

- The Attending Physician's Statement (APS): The insurance company requested complete medical records directly from her primary care physician to verify her stability.

- The Tele-Underwriting Interview: A nurse called my aunt for a 30-minute phone interview to verify her cognitive health, mobility, and daily living capabilities.

The Mistake We Almost Made

During the questionnaire phase, my aunt wanted to omit a brief hospital observation stay from three years prior, thinking it "wasn't a big deal."

I stopped her. Omitting medical history on an insurance application is considered material misrepresentation. If the insurer discovers it later through medical records, they can legally cancel the policy and reject all outstanding claims (Source 2). We disclosed everything.

The Real Outcome

Because of her controlled mild arthritis and thyroid condition, she was not rejected, but the insurer applied a premium loading—meaning her monthly rate was 15% higher than the standard preferred rate. However, securing that Medigap plan gave her unlimited access to specialists without needing referrals, which was her primary goal.

The Hidden World of Ancillary Benefits: Wellness Programs & Telehealth

When I first helped my parents sign up for their private senior health plan, I completely ignored the glossy brochures explaining the "extra benefits." I assumed they were marketing gimmicks.

I was wrong. Over the last few years, these ancillary benefits have saved my family thousands of dollars and significantly improved my father's quality of life.

The Telehealth Revolution

During a harsh winter, my father developed a severe skin rash. Instead of bundling him up and driving through freezing rain to a clinic, we opened his insurer's mobile app and initiated a telehealth consultation (Source 1).

- The Experience: Within ten minutes, we were speaking face-to-face with a board-certified dermatologist via video.

- The Outcome: The doctor diagnosed the shingles outbreak, electronically sent a prescription to our local 24-hour pharmacy, and we had his medication in hand within two hours. The copay for the entire virtual visit was $0.

- The Lesson: For seniors with mobility challenges or those living in rural areas, robust telehealth services are not just a convenience—they are a clinical lifeline (Source 1).

Wellness Programs and Active Aging

Another massive benefit we unlocked was the built-in wellness programs offered by modern private carriers like Oscar Health, Ambetter, and UnitedHealthcare (Source 1).

- SilverSneakers and Gym Memberships: My father's plan includes a free membership to a local wellness center, which features specialized senior water aerobics and strength training classes. These programs often focus on promoting preventive care services and chronic disease management.

- Cash Rewards for Healthy Habits: Some tech-forward plans actually pay you to stay healthy. By syncing his pedometer to his health insurance app and completing his annual wellness exam, my father earned $200 in digital gift cards, which we used to purchase his blood pressure monitor.

Long-Term Care and Aging in Place: Planning for the Unthinkable

No one wants to talk about the day when they, or their loved ones, can no longer bathe, dress, or feed themselves, requiring specialized geriatric care. But ignoring this reality is the fastest way to deplete a lifetime of savings.

When my grandmother's cognitive health began to decline, we had to quickly evaluate how to fund her care. We wanted her to age in place in her own home, but the cost of private in-home sitters was astronomical.

The Harsh Truth About Medicare and Long-Term Care

The biggest myth in senior healthcare is that Medicare pays for nursing homes or long-term assisted living. It does not.

Medicare only covers skilled nursing care on a short-term basis (up to 100 days) if you are recovering from an acute illness or injury, such as a hip replacement (Source 2). If you need custodial care (help with daily activities), you are entirely on your own.

Navigating the Texas HHS Long-Term Care Programs

Because my grandmother lived in Texas and had limited financial resources, we turned to the Texas Health and Human Services (HHS) department for help (Source 3).

- Community Care Services: Through Texas HHS, we applied for programs that assist with daily tasks, allowing her to stay in her home longer (Source 3). This included home-delivered meals, emergency response systems, and minor home modifications (like installing grab bars in her bathroom).

- Medicaid Spend-Down: To qualify for long-term Medicaid assistance, we had to navigate the complex "spend-down" process, ensuring her assets met state-mandated limits without violating the five-year Medicaid look-back period.

My Advice for Families Facing This Transition

Based on my personal experience navigating this emotional and financial minefield, here are the steps you must take today:

- Have the Conversation Early: Talk to your parents about their wishes for long-term care before a medical crisis forces your hand.

- Consult an Elder Law Attorney: Before transferring assets or applying for state Medicaid benefits, consult a certified elder law attorney to protect your family's estate.

- Audit Your Local State Programs: Research what specific aging services are offered by your state's health department, as programs vary wildly from state to state (Source 3).

References

-

Seniorstrong — Top Medical Insurance Options for Senior Citizens, 2026

-

Joinditto — Health Insurance For Senior Citizens: Top 5 Plans – June 2026 – Ditto, 2026

-

Hhs — Programs for Seniors & Aging – Texas Health and Human Services, 2026

-

Uhc — Health insurance for individuals & families | UnitedHealthcare, 2026

-

Careinsurance — Senior Citizens Health Insurance: Best Medical Insurance for 60+, 2026

-

Forbes — Best Health Insurance For Retirees – Forbes Advisor, 2026

-

Cignaglobal — International Health Insurance for Seniors | Cigna Healthcare, 2026

-

Hdfcergo — Senior Citizen Health Insurance Plans, 2026